Europe is winning ground, and is done renting its tech stack.

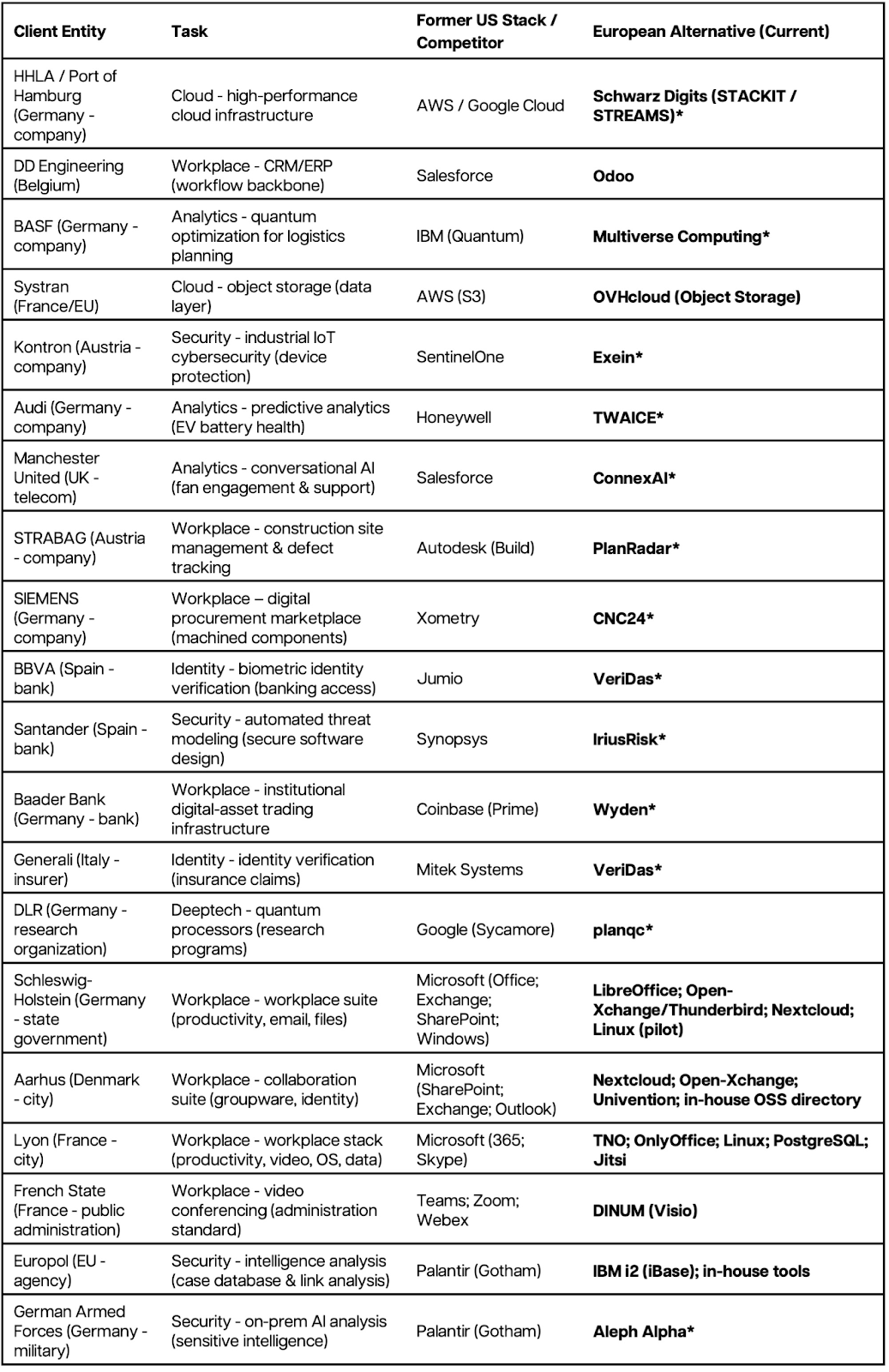

Across Europe, a structural shift is underway. Cities, countries, and enterprises are implementing a sovereign European tech stack. From Schleswig-Holstein moving away from Microsoft services, to Aarhus and Copenhagen adopting open-source collaboration platforms, to Systran and Hopsworks shifting workloads from AWS to OVHcloud, these are no longer isolated experiments. They signal a broader reorientation toward European technological sovereignty.

This is not symbolism. It is a pragmatic recalibration of critical digital infrastructure.

At its core, this shift is about sovereignty and control. When critical digital infrastructure is governed outside Europe, institutions operate within external legal and geopolitical frameworks. The goal is not abrupt decoupling, but restoring leverage, optionality, and strategic autonomy.

The economic stakes are significant: with Europe’s total IT spending forecast at ~€1.09tn in 2025, even a 1% redirection toward European suppliers would shift roughly €11bn per year onto European balance sheets.

The Shift in Motion

* ASTRA investment, supporting European sovereignty and competitiveness. Astra is a consortium consisting of 360 Capital, Bullhound Capital, Redstone, Truffle Capital, UVC Partners, and 28Digital.

Economic and Ecosystem Implications

After sovereignty and dependency, cost reinforces the case. Licensing inflation and cloud pricing pressure accelerate adoption.

More importantly, redirecting public-sector and enterprise demand toward European providers strengthens the European tech ecosystem. Each move toward LibreOffice, Nextcloud, OVHcloud, Matrix-based messaging, or other European solutions contributes to scale, recurring revenue, and reinvestment capacity within Europe.

This directly supports a broader structural ambition: Europe cannot build global champions without demand at home. Sovereign procurement and enterprise adoption create that demand.

Facts

Europe’s cloud market is projected at roughly €74.4bn in 2025, yet it remains highly concentrated: AWS, Microsoft, and Google account for ~70%, while European providers hold only ~15% share. A shift from 15% to 25% would imply ~€7.4bn per year redirected within Europe (and ~€11.2bn at 30%).

An EC-commissioned Fraunhofer ISI study estimated that EU firms invested ~€1bn in open source in a 2018 baseline year, associated with €65-€95bn in economic impact and a cost-benefit ratio above 1:4. It also modeled that a 10% increase in open-source contributions could add +0.4% to +0.6% to EU GDP annually and generate 600+ additional ICT startups.

With Europe’s total IT spending forecast at ~€1.09tn in 2025, even a 1% redirection toward European suppliers would represent ~€10.9bn per year shifting onto European balance sheets.

The Core Driver: Strategic Sovereignty

In nearly all cases, the primary justification is sovereignty. Danish municipalities explicitly referenced the risks of excessive dependence on a single US vendor. French authorities framed Visio and Tchap as ways to avoid relying on “extra-European” platforms for sensitive public communications. Schleswig-Holstein presented its initiative as a move toward a “Microsoft-free workplace” to reduce structural lock-in.

The concern is not performance. It is control. When core communication systems, collaboration tools, cloud infrastructure, or document standards are governed by non-European actors, institutions operate within external legal and geopolitical frameworks. Digital infrastructure has become strategic infrastructure. Sovereignty now includes software.

Reducing Structural Dependency

Many of these transitions are designed to introduce optionality. Aarhus structured interoperability between Microsoft and open-source environments during its transition. Schleswig-Holstein is replacing components in stages (email, office suite, collaboration, then operating system) to regain leverage and reversibility.

The objective is not abrupt decoupling. It is restoring strategic flexibility. This brick-by-brick approach reflects lessons from earlier large-scale migrations: continuity and operability matter. The shift is pragmatic, incremental, and execution-focused.

Operational and Political Consequences

The consequences extend beyond procurement.

Operationally, European institutions regain control over data jurisdiction, hosting models, interoperability standards, and roadmap alignment. Politically, they reduce exposure to extraterritorial regulation and geopolitical volatility. Digital dependence is no longer merely technical. It is a matter of governance capacity.

Europe is not rejecting global technology. It is rebalancing it.

A Structural shift, Not an Anecdote

What makes this moment significant is repetition. The same motivations recur across cases: sovereignty and jurisdictional control; reduced single-vendor dependency; strategic flexibility and reversibility; strengthening European technological capacity.

The question is no longer whether European alternatives exist. They do. The question is whether Europe will choose to scale them systematically.